B2B Payment Terms: Why Every Invoice Is a Credit Decision

Net-30. Net-60. Due on receipt. Most finance teams treat B2B payment terms like a default setting, creating friction between the buyer and supplier.

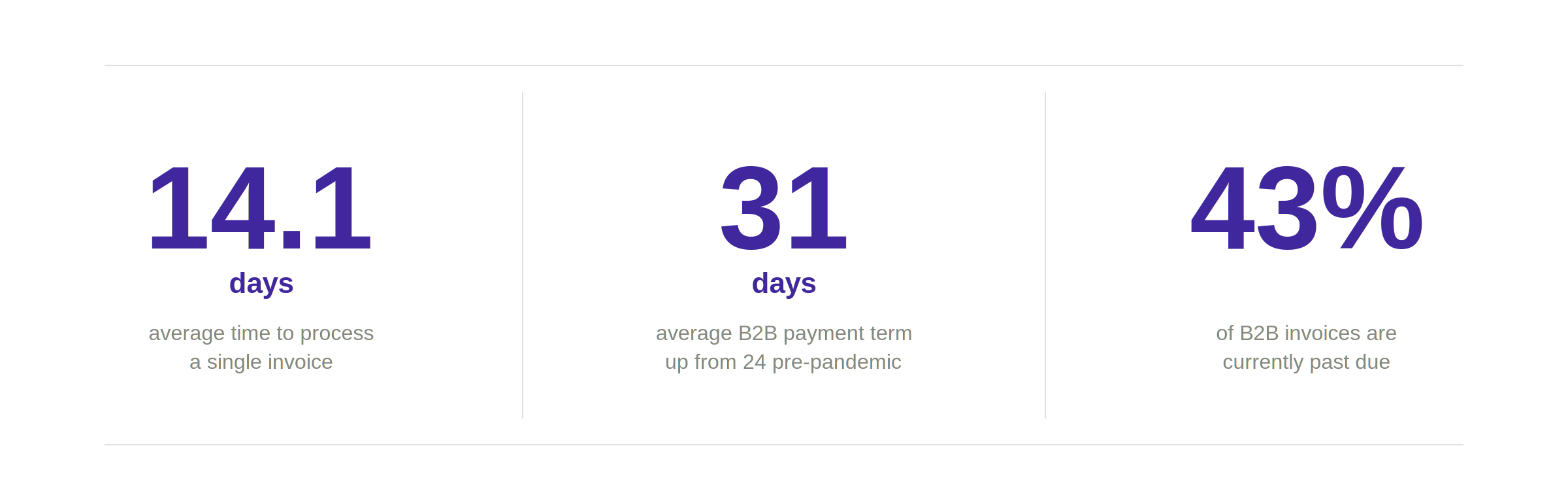

48% of businesses transact online with thousands of suppliers and buyers, and the average invoice takes 14.1 days to process. The average B2B payment term is now 31 days, up from 24 pre-pandemic, and 43% of B2B invoices are currently past due (18% jump since 2019).

Here's what that framing misses: every payment term is a credit decision. When a buyer and supplier agree on Net-45, they've just structured a 45-day unsecured loan. There is no credit check, no explicit risk pricing, no one acknowledging what actually happened.

The foundation of every B2B transaction is trust.

And when a buyer is transacting with hundreds of suppliers online, that trust doesn't scale.

What B2B Payment Terms Actually Are

B2B payment terms define when a buyer pays a supplier after delivery. The common structures:

Net Terms – payment due within a fixed number of days after invoice. Net-30, Net-45, and Net-60 are standard across most industries.

Dynamic Discounting – written as "2/10 Net-30": 2% off if paid within 10 days, full amount due in 30. Suppliers trade a small margin for faster cash. Buyers capture a discount for deploying capital early. When managed systematically across a supplier base, dynamic discounting becomes a working capital lever.

Credit Cards and Commercial Charge Cards – some buyers pay suppliers via corporate card, effectively converting an invoice into a card transaction. The buyer gets a billing cycle buffer and rewards. The supplier absorbs 2–3% interchange.

Every Invoice Is Essentially an Unsecured Loan

When a supplier ships goods on Net-30, they've essentially extended a 30-day unsecured loan equal to the invoice value. The supplier is the creditor. The buyer is the debtor. There's a contractual obligation to pay a defined amount on a defined date. If the buyer doesn't pay, the supplier absorbs the loss.

That's hidden credit. The only thing missing is the formal infrastructure: underwriting, automated funding, and servicing.

Most B2B payment terms skip all of it. Suppliers extend terms based on the commercial reality that refusing terms means losing the customer. When payment runs late – which affects 55% of the total value of B2B invoices in the U.S., per Atradius – both sides absorb the damage.

The DPO/DSO Conflict at the Core of Every Transaction

Every B2B invoice sits at the intersection of two metrics pulling in opposite directions.

Days Payable Outstanding (DPO) – how long a buyer holds cash before paying. Higher DPO improves the buyer's working capital and free cash flow.

Days Sales Outstanding (DSO) – how long a supplier waits to get paid. Lower DSO means faster cash conversion and less credit exposure for the supplier.

Every invoice is a structural negotiation: the buyer wants to extend DPO, the supplier wants to compress DSO, and payment terms reflect whoever has more leverage.

This conflict doesn't resolve through better invoicing software or faster approval workflows. It only resolves when a third party steps in to absorb the gap – paying the supplier early while extending the buyer's payment horizon, and pricing the risk in between. That's what working capital infrastructure does. And it's what most B2B payment platforms still aren't offering.

How This Plays Out Across Industries

The DPO/DSO tension shows up differently depending on the sector:

Travel and Booking – Platforms like Sabre manage enormous B2B payment flows between travel buyers and suppliers, with virtual card programs dominating the rails. The catch: suppliers absorb 2–3% interchange on every transaction and deal with inconsistent settlement windows.

Freight and Logistics – Carriers and shippers operate on stretched Net-30 to Net-60 terms in an industry where fuel, driver pay, and equipment costs are immediate obligations. Quick-pay programs exist but are typically off-platform and expensive for what is fundamentally a short-duration credit product.

FreightOS has demonstrated what it looks like to modernize freight payment infrastructure; the opportunity for platforms in this space is replacing manual reconciliation and costly quick-pay programs with automated, network-aware settlement.

Contingent Workforce – Staffing agencies and workforce platforms pay workers weekly while clients settle on Net-30 to Net-60. Platforms like Papaya Global, which manages contractor payments and compliance across global workforces, sit on top of this problem at scale.

Professional Services – Net-30 is standard on paper; actual payment behavior is another story. Project-based firms routinely deal with DSO creep as clients dispute deliverables or simply deprioritize invoices.

Platforms like Lawtrades, which manages legal workforce management and invoicing, manage this tension. Their suppliers (attorneys and legal professionals) need predictable payment while their buyers (corporate legal teams) operate on standard enterprise payables cycles.

Healthcare and Insurance – On platforms like GHX, Net-60 to Net-90 is the norm, driven by complex procurement approval, supply chains, and reimbursement cycles.

Flychain has carved out a niche specifically solving working capital for healthcare providers caught between long reimbursement cycles and immediate operational expenses.

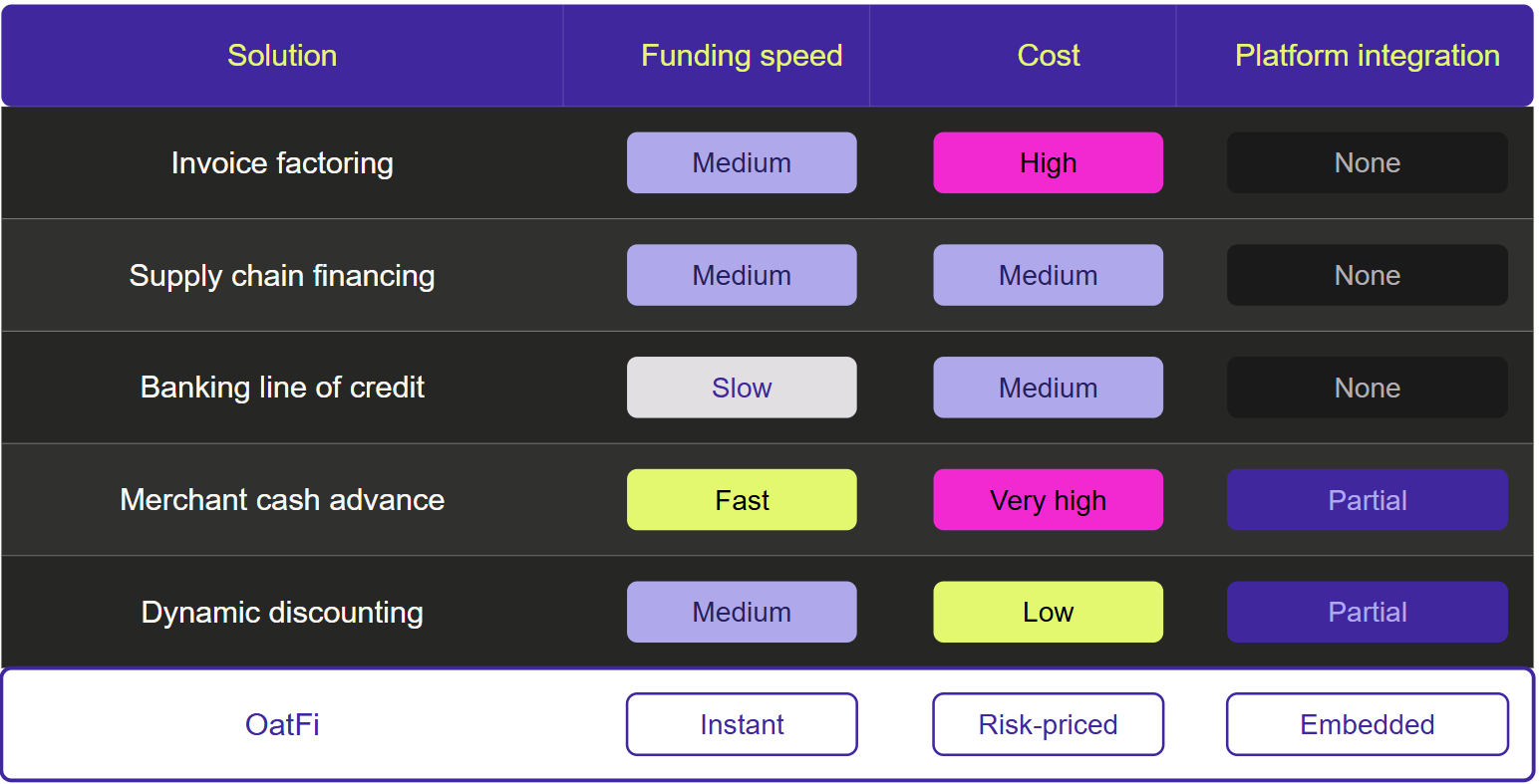

How Businesses Try to Fix It – And Why Most Solutions Fall Short

Businesses have developed a set of workarounds. The problem: almost all of them are off-platform, create friction, carry poor economics, and treat the symptom rather than the cause.

Invoice Factoring – a supplier sells outstanding receivables to a third-party factoring company at a discount in exchange for immediate cash. Off-platform factoring companies base rates on generic credit assessments rather than actual buyer-supplier payment history. And because factoring happens entirely outside the platform where the invoice originated, there's no reconciliation benefit.

Supply Chain Financing – a buyer arranges financing through a bank, allowing suppliers to get paid early against the buyer's credit rating. It only works for suppliers large enough to matter to the buyer, requires a direct program setup between buyer and bank, and excludes the long tail of smaller suppliers.

Banking Lines of Credit – many businesses plug their working capital gap with revolving credit lines. It works, but it's expensive relative to the underlying transaction risk, requires periodic requalification, and does nothing for the reconciliation problem.

Merchant Cash Advances (MCAs) – MCAs provide upfront capital in exchange for a percentage of future receivables, structured as a daily or weekly repayment drawn directly from a bank account. They're fast and accessible, which is why they're common among suppliers who can't qualify for traditional credit. But the economics are punishing. Effective APRs frequently run 40–150%.

Dynamic Discounting – buyers offer suppliers early payment in exchange for a discount, funded from the buyer's own surplus cash. While reasonable when the buyer has liquidity, it requires the buyer to actively manage the program, limits access to suppliers the buyer has chosen to prioritize, and disappears the moment the buyer's cash position tightens.

The traditional credit system isn't filling the gap. Only 44% of SMBs report having access to adequate financing and working capital solutions. In 2023, the share of firms applying for loans, lines of credit, or merchant cash advances actually declined due to accessibility barriers. The SMB lending market is expected to grow at 13% annually to $8 trillion by 2032, but the businesses that need capital most are the least likely to get it through traditional channels.

What OatFi's Infrastructure Does Differently

With OatFi, the platforms redefining B2B payment terms recognize that every B2B payment is a credit transaction.

Instead of leaving both sides to negotiate an adversarial outcome, a liquidity and reconciliation layer acts as counterparty to both simultaneously. Suppliers get paid immediately (Early Pay) or on a guaranteed due date (Guaranteed Payment). Buyers get to still pay on net terms.

OatFi acts as the trusted transaction layer — authorizing and reconciling the invoice, establishing a payment obligation, and inserting liquidity into the point of payment. That event allows buyers and suppliers to transact with confidence.

This is the model OatFi's B2B payment network is built on. The AP or AR platform's existing approval workflow becomes the trust anchor for the entire settlement mechanism. No new buyer behavior is required.

What This Means If You Run a B2B Platform

Platforms that add embedded finance to their payment flows convert a process tool into a revenue channel. Buyer retention increases because the platform now owns their entire payables and receivables workflow. Supplier loyalty follows because guaranteed payments eliminate the uncertainty that pushes suppliers off-platform.

The platforms that treat every invoice as a credit decision will build the infrastructure to match. The ones that don't will lose out on the ability to monetize every B2B transaction.

Turn your B2B payment platform into a revenue engine. Talk to OatFi →

1. PYMNTS — "The Invoice Innovation That's On The Roadmap Of 75 Percent of AP Professionals"

2. AFP — "2019 Electronic Payments Survey"

3. FIS Global — "2019 Corporate Liquidity and Bank Connectivity Market Report"

4. Atradius — "US: Business Environment Strained by Cash Flow Issues"

5. PYMNTS — "Study Finds Cash Flow Crisis Deepening for Small Businesses Amid Tariffs and Consumer Pullback"

6. Canopy — "The State of Small Business Lending: Statistics and Trends for 2025"

Explore how OatFi partnered with these businesses

Ready to get started? Get in touch.